Homes are Emotional Investments

... not Financial Assets

Welcome back to the Rambling Mind Newsletter.

This post is 1331 words and 8 min read. Enjoy!

Before we get into the topics for the day, if you have a quick minute please fill out this short survey. It will take no more than 2 minutes. This will enable me better know who my audience is and the content to create for y'all. Thank you!

Two charts from Ben Carlson totally ruined my week.

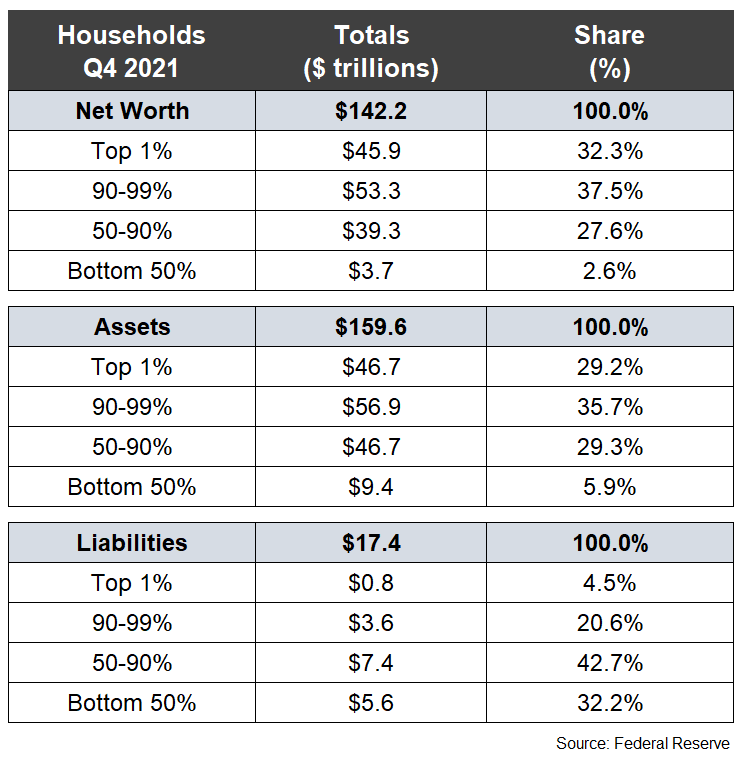

The first chart shows the US households, that own the assets and debts in the United States.

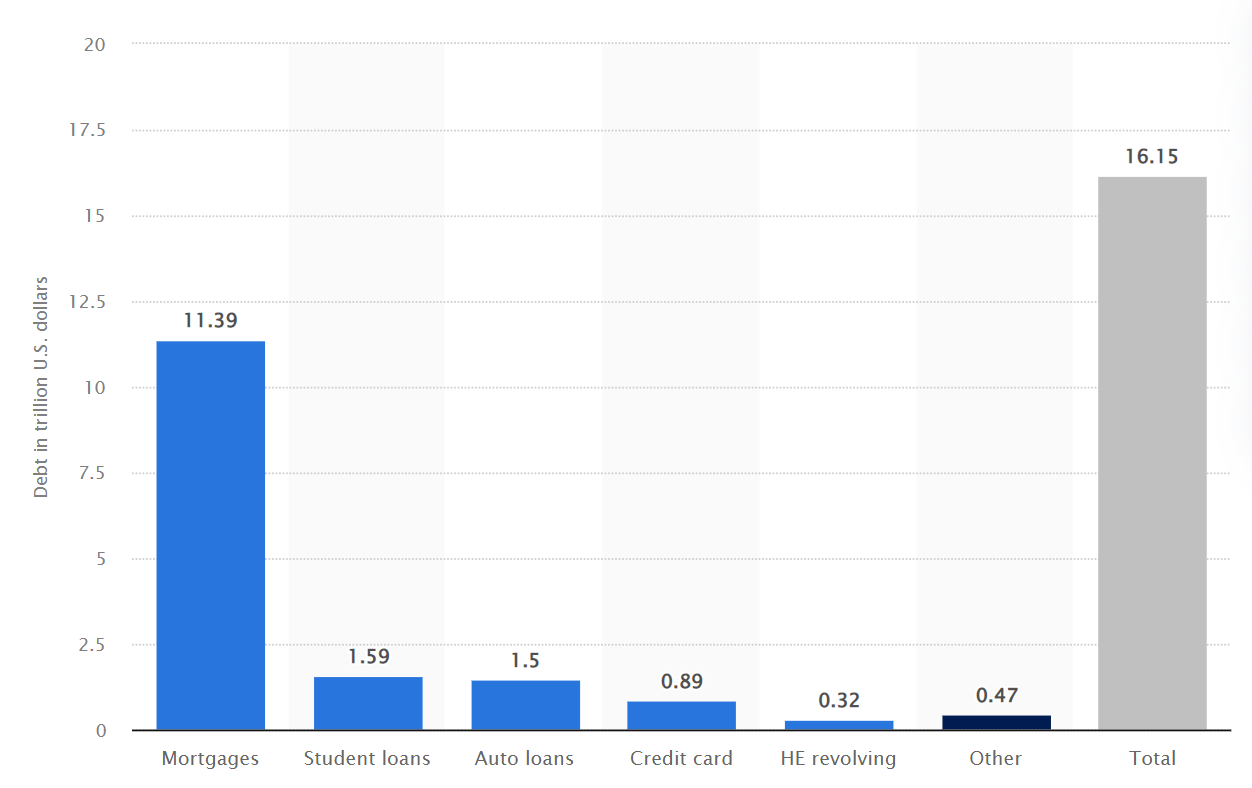

The second chart shows how those assets are broken down

They absolutely rocked my world.

I could not understand how almost all the assets (~70%) are owned by just 10% of the population. However, most of the debt (~75%) is owned by the remaining 90%. It absolutely blew my mind but then I remembered an old saying:

One man's debt is another man's asset.

And when we dig deeper, we see exactly where the division lies:

As of the third quarter of 2022, the total US household debt was $16.5 Trillion.

$11 Trillion was from mortgages.

When we look at a breakdown of who owns what kind of assets (as shown above), the top 10% has a smaller exposure to Real Estate than the bottom 90%.

The takeaway is the bottom 90% of US households' only asset for building wealth is real estate. Typically this is their primary residence. This poses a very dangerous situation.

As Nobel Prize laureate Harry Markowitz said "Diversification is the only free lunch in investing." Having all your eggs in one basket is never a good plan. But also, a house is a leveraged (secured by debt) asset. Meaning if anything happens, it can be taken away from you. This makes it the largest liability not only by dollar amount but also the largest mental liability a person can have.

This is never the picture that is painted, whenever there is a discussion on purchasing a home. The picture being painted is always one of the joys of home ownership. The freedom of home ownership. And the biggest picture that is painted:

A HOUSE IS AN INVESTMENT!

Why pay rent and throw money away, when you can build equity in your own home? Plus, you never lose money in Real Estate.

Today, I am tearing this picture apart.

It is a lie that is designed to get you and I emotionally activated and to ignore the actual costs of home ownership. It always seems to come with anecdotal stories of someone we all know, who bought a house back in 1992 for $100,000 and just sold it for $500,000.

By no means am I trying to convince you of anything. It will take much more than a blog post to counter decades of advertising and propaganda that has become common knowledge. But I do want us to open our eyes to see what we walk into when we make the largest financial expense of our lives.

So let’s break down the “Amazing Investment" turning $100,000 into $500,000:

There are many phantom costs to ownership that people never mention.

Let’s begin with property maintenance and upkeep over the 30-year ownership period:

Typically, you can estimate that it will cost you about 2-5% per year to maintain the house: $1000/year (I am not factoring inflation into the cost which would add another 2-3% increase in cost per year)

So we can estimate $30,000-$45,000

Also, you'll have to replace things like the water heater, roof, HVAC, foundation, etc.

We can estimate every 10 years spending at least $20,000-$25,000. Which would be about $60,000 to $100,000 over 30 years.

How I reached the numbers:

A roof replacement costs at least $10,000, you need one every ~10 years

HVAC usually needs to be replaced every ~7 years and costs about $5,000-$7000

Water heaters need to be replaced every 10-15 years and cost about $4,000-$5,000

There is also the interest you pay during the life of the loan. Remember your interest costs are front-loaded, you don’t really get to build equity until the back end of the loan:

In 1992 the average 30-year fixed mortgage rate was 8.39%

So over the life of the loan, you would have paid $174,007 in interest

Side note: this is why the interest rate is more important than the principal of the house.

There are also service costs to buy or sell a house:

When purchasing, you pay anywhere from 3-6% of the loan: $3,000 to $6,000

When selling, you pay anywhere from 6-10% of the loan: $6,000 to $10,000

Miscellaneous expenses for inspections etc.: $2,000-$3,000

You also have the annual taxes paid on the property. This is very state, city, and county dependent but the national average on real estate taxes in the US is about $2,578:

Over 30 years, it is $77,840. Let's estimate $70,000 to $80,000

When you add everything up, the house ends up costing you between $445,000 to $518,000. Remember the house was sold for $500,000, which on face value alone seems like an "Amazing Investment".

I am sure there are a ton of holes that can be poked in my calculations but this was just to give an idea of what the true cost of home ownership can be.

When I think of locking my money up for 30 years, I am looking for much better financial returns.

Warren Buffett, the Greatest Investor of our generation, told this story when asked about buying a home:

I'll just relay one story, which was when I got married we did have about $10,000 starting off, and I told Susie, I said, "Now, you know, there's two choices, it's up to you. We can either buy a house, which will use up all my capital and clean me out, and it'll be like a carpenter who's had his tools taken away for him. "Or you can let me work on this and someday, who knows, maybe I'll even buy a little bit larger house than would otherwise be the case." So she was very understanding on that point. And we waited until 1956. We got married in 1952. And I decided to buy a house when it was about -- when the down payment was about 10% or so of my net worth, because I really felt I wanted to use the capital for other purposes.

Now I am not saying "DO NOT BUY A HOME".

There are plenty of benefits to owning a home:

Consistency and Predictability with the monthly payment

Shelter and Safety

Memories

Emotional Joy of Gatherings

Freedom

For my entrepreneurial folks:

Rent

Leverage

Taxes

Inflation

Homes can be great investments but not typically by financial standards. They are great Emotional Investments, which can be more important.

So if you want to buy a house, buy a house. I mean I DID!

But before you do decide to buy a house, RUN THE NUMBERS! Do not buy a house because you have been told, “A home is the best path to build wealth.”

Buy a home because it fits your current needs and you can actually afford it. By that, I do not mean just the down payment but can afford to OWN the house and all the COSTS that come along with it.

Thanks for reading

Remember GENEROSITY > greed

✌🏾

Recommended Reads

Starting a new section in the newsletter of things that I read that I enjoyed and you might as well:

Nick Maggiulli gives an easy breakdown of how to think about your investment returns over the long run

Morgan Housel shares some of the Ideas that have forever changed his life

Josh Brown breaks down how the US Economy functions for a select group but COVID broke that cycle and revealed what it would take for everyone to succeed.

Money With Katie breaks down just how $100 will cost you $30,000

Jack Raines breaks down the different types of wealth and why we might need to prioritize none financial wealth that we cannot see.