It's Leaking - Market Update Jan 27-31, 2025

Maybe just a bit

This newsletter is 3,281 words a 15-min read

Reply to this email with your thoughts about any of the topics discussed. I love hearing back from readers and will include those in a new section of the newsletter.

Welcome back to the Rambling Mind Newsletter. This is your Market Update.

Summary of Topics:

Economic News

🫧AI Bubble Pops

✂️No Rate Cut

🪖Trade War begins

Company News

ASML Earnings: Back on Track

Microsoft Earnings: Nothing Has Changed

Facebook Earnings: Zuch feeling himself

Tesla Earnings: It's All a Story

Apple Earnings: Becoming like Walmart

Stats of the Week

💳10.75% Minimum

💵4% or Less

🏈$8 Million for an ad

📈15% More Increases

Looking Ahead

Jobs

More Earnings

Sports I Love

Man U does the Man U

Craziest Trade

Extras

Reading Levels Keep Dropping

Markets

No time for a preamble. We got a lot to cover. Let’s get into it.

Year To Date Returns

Tale of the Tape

Economy

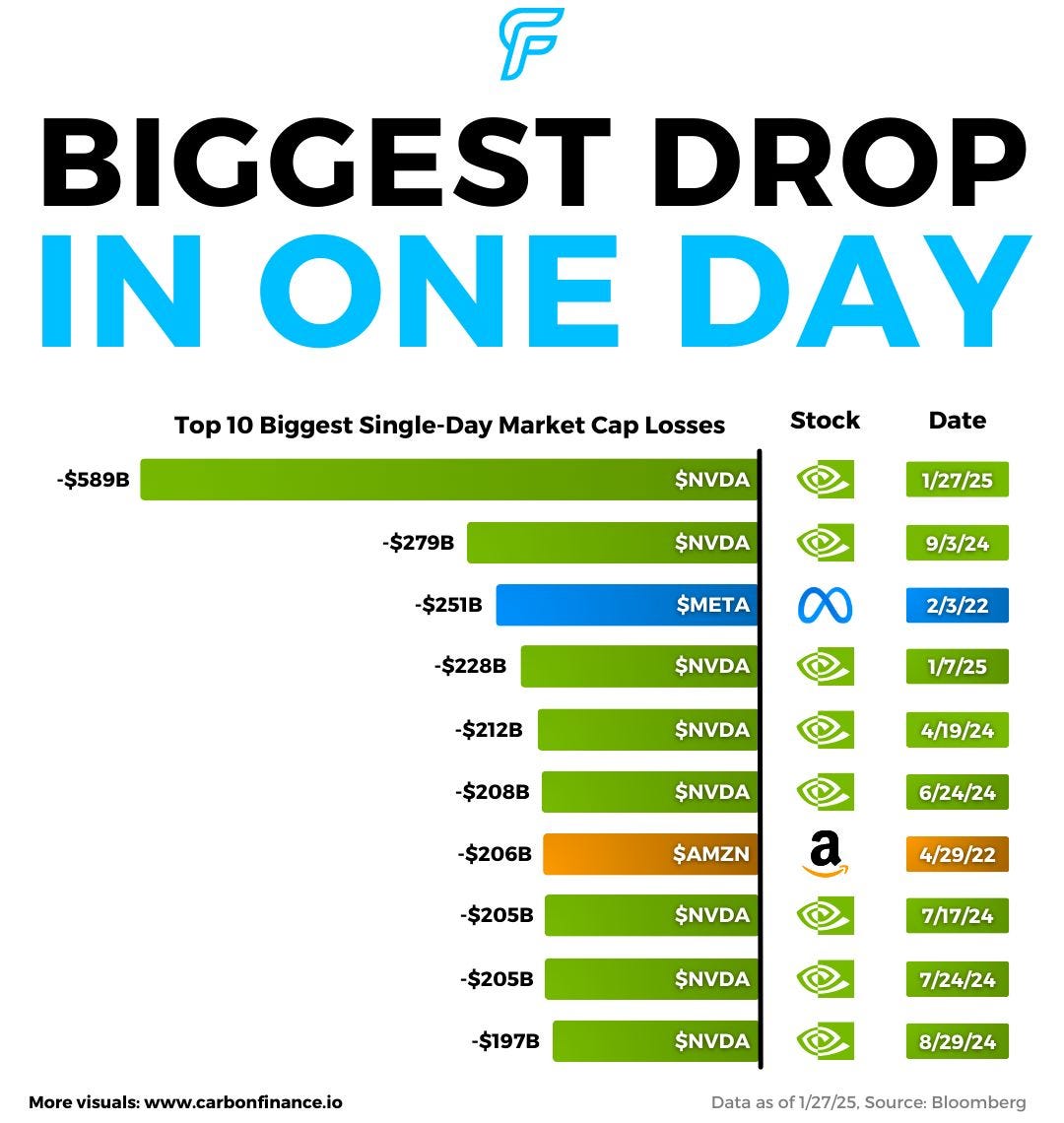

People have been looking for a reason to worry about these tech companies and they might have finally had their confirmation.

🔎Details: Two weeks ago, a company called DeepSeek released their version of an AI chatbot to the public. In less than one day, the largest tech companies that are focused on AI lost almost $1 trillion in value.

DeepSeek is a Chinese start-up that similar to OpenAI and Anthropic, has been researching and building out its large language model. The belief was all Chinese LLMs were years behind the United States due to limitations in the chipset that these companies could use. The US has banned all chipmakers from providing any Chinese firms with the latest and most powerful processing chips used in AI.

On Thursday, DeepSeek released an app on both the Apple Store and the Google Play Store. It quickly dethroned OpenAI and appears to outperform OpenAI's ChatGPT, Anthropic's Claude, and Meta's Llama.

The kicker was unlike OpenAI and Anthropic, DeepSeek's app and language model is a free, open-source platform.

🔢By The Numbers: DeepSeek said it spent $6 million to train its model.

Compared to the other 3 which have spent almost $1 trillion on training and developing AI models over the last 5 years.

And are projected to spend almost $300 Billion this year alone.

😶Takeaway: This shows how much the market sits on pins and needles. The market has so much hope priced into these large tech companies that anything that goes against the expected will cause a complete route. Especially for companies like Nvidia, which saw the largest decline. Falling over 25% ($600 Billion in market cap lost), in one day.

The market and economy is relying heavily on the hopes of an AI-expensive future. If that future does not pan out as expected, there will be a lot of pain in the markets.

😒My Takeaway: Someone is LYING!! There is no way they spent $6 million to train this model. Something about this whole thing just seems fishy and weird. But if true, it would be great news for all the companies currently reliant on Nvidia chips. Hence the quick recovery for most of these stocks.

Regardless, it is showing that having an AI model might not be a defendable MOAT for companies. It shows that it is likely that those who will benefit from these technologies might not be the creators but rather the service built on top of them. Example: it is not Comcast & AT&T that benefit the most from the internet. It is Facebook, Microsoft, and Netflix that are benefitting the most. It might be a similar story for AI.

To the surprise of absolutely no one, Papa Powell last Wednesday announced that the Fed Funds Rate will remain between 4.25% and 4.5%.

🔎Details: Powell and the Fed are still worried about inflation. Although it has subsided a good amount, inflation has stubbornly remained above their 2% target. Core PCE in November was 2.8%, and the estimates for December is about the same. Giving no reason for the Fed to push rates any lower.

💬In His Words: Powell told reporters at the press conference, "The central bank will need to see real progress on inflation or some weakness in the labor market before we consider making adjustments. With our policy stance significantly less restrictive than it had been, and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance."

😲The Intrigue: This sets a direct crash course with President Trump, who announced at Davos that he will demand lower rates.

Takeaway: Expect a lot of bloviating from President Trump about Papa Powell in the coming days. Because he not getting what he wants from the Fed.

Powell was asked about this and he said, “focusing on using our tools to achieve our goals and keeping our heads down and doing our work.”

On Sunday, President Trump posted, "THIS WILL BE THE GOLDEN AGE OF AMERICA! WILL THERE BE SOME PAIN? YES, MAYBE (AND MAYBE NOT!). BUT WE WILL MAKE AMERICA GREAT AGAIN, AND IT WILL ALL BE WORTH THE PRICE THAT MUST BE PAID."

🔎Details: Trump enacted the "Tariffs to Protect Americans". It places a 25% tariff on Canada and Mexico and a 10% tariff on China.

Shortly after the announcement, Canadian Prime Minister Justin Trudeau announced retaliatory tariffs of 25% on US exports including beer, goods, and manufacturing products.

Trudeau also encourages Canadians to buy from local producers and avoid visiting the US for vacations.

Expect China& Mexico to announce their retaliatory tariffs shortly.

🔢By The Numbers: After kissing Trump's butt since he took office. Businesses are panicking and announcing the negative effects it'll have on American families.

The Tax Foundation (a conservative think tank) said the tariffs will effectively be a tax of $830/year on the average US household.

Takeaway: How these tariffs will protect Americans is yet to be seen. What is known is that these tariffs will increase the cost of everyday items. So expect life to get a good bit more expensive as companies find ways to pass the cost of price increases to you and me.

Trump has ushered in an era of trade war not seen in decades. The precious times presidents have gone down this road, it has never protected Americans. Maybe this time it'll be different.

But I highly doubt it.

Companies

My newest holding as of sometime late last year when there was a bit of panic around the company. Reported earnings on Wednesday, and it was business as usual. Despite all the fears brought on by DeepSeek challenging the existing AI players.

📈Stock Move After Earnings: The stock Ripped 11% after the report.

By The Numbers: The most important number for ASML is its quarterly/annual bookings. ASML reported that bookings grew to €7.1 billion, more than doubling from the €2.6 Billion it had in Q4 2023.

ASML reported revenue of €9.3 billion in Q4, 2024. 28% growth from 2023.

Profits increased 30% to €2.6 Billion

Gross margin expanded to 51.7% from 50%

💬In Their Words: ASML CEO Christophe Fouquet told investors, "Consistent with our view from the last quarter, the growth in artificial intelligence is the key driver for growth in our industry. It has created a shift in the market dynamics that is not benefiting all of our customers equally, which creates both opportunities and risks as reflected in our 2025 revenue range."

Takeaway: Business as usual. ASML has no reason to panic or change anything they are doing.

👀What to Watch: How does the booking number change now that it seems a ton of commute might not be needed in the future?

ASML is forecasting between €30 billion and €35 billion in revenue for this year. In line with, the bookings they estimated for at the end of last year.

It will be important to keep an eye on that number as companies digest the latest information from DeepSeek.

My Take: As an ASML investor, I have no worries about the potential that ASML tools will be needed in the future. Regardless of what happens with DeepSeek, using chips more efficiently does not eliminate the higher demand for data centers. Which means ASML will still need to make its machines. The only worry I have is when a competitor shows up with a better way of doing things.

Explaining Obscure Financial Terms

Bookings are a metric that measures the value of new contracts or orders that a business has received but not yet fulfilled (according to Investopedia).

It is like getting someone to come paint your house and you agree to a date and time but no money or service exchanges hands until the work has been done.

Takeaway: Big spending on AI continues. Revenues still growing double digits but investors are unhappy with slightly slower revenue growth projects.

📉Stock Move After Earnings: The stock tanked 5% after earnings.

🔢By The Numbers: Revenues grew 15% to $69 Billion for Q4 2024, and profits increased 10% to $24.1 Billion.

The fastest growing segment for Microsoft, Azure Cloud, grew "only" 31% in the quarter versus 34% in the prior quarter.

Microsoft projected revenues of $67.7 to $68.7 billion versus analysts' estimates of $69 Billion. A 12% percentage growth.

Microsoft invested $22 Billion in Q4 on AI Capital expenditure. More than double what it had spent the year before.

💬In His Words: CEO Satya Nadella said on the earnings call, “We are innovating across our tech stack and helping customers unlock the full ROI of AI to capture the massive opportunity ahead. Already, our AI business has surpassed an annual revenue run rate of $13 billion, up 175% year-over-year.”

My Take: Investors are children. Expectations are far too high for a lot of these tech companies. And this company makes so much damn money.

👀What to Watch: When will CapEx spending slow down and free cash flow begin growing again?

Takeaway: Pretty much the same as Microsoft. Revenues up, profits up, forecast down but investors loved Meta. Cause the growth rate was much larger.

📈Stock Move After Earnings: The stock ripped 4% after earnings.

By The Numbers: Revenue grew 21% in the 4th Quarter to $48 Billion. Profits increased 49% to $20 Billion.

It expects revenue for Q1 2025 to be between $39.5 to $41.8 Billion. Right at the $41.7 Billion mark analysts project

Zuch announced an additional $60-$65 Billion of Capex this year.

💬In His Words: Zuch said on the call, “I would bet that the ability to build out that kind of infrastructure is going to be a major advantage for both the quality of the service and being able to serve the scale that we want to.”

Interpretation: We gonna be spending massively for a while.

My Take: This explains why Zuch has been feeling himself a lot more lately. He is making so much money. He has the Midas touch and is rocking with it.

👀What to Watch: Zuch and Facebook are in a great position. DeepSeek helped establish the strength of Meta's Open Language Model as potentially far stronger than closed-off models like OpenAI. But how long does that advantage last for? When will investor's patience run out?

Tesla

Takeaway: This company is simply a story. A story that is extremely loved by investors, despite not-so-great numbers.

📈Stock Move After Earnings: Stock ripped 4.31% after hours.

🔢By The Numbers: Total revenues increased 2% to $25 Billion. Profits fell 71% from a year ago to $2 Billion.

Car revenues fell 8%

Gross margin continues to decline, it was 6.2% from 8.2% the last year.

Total car deliveries in 2025 declined to 1.8 million

💬In His Words: Elon made many promises on the call. A few examples:

“we expect the vehicle business to return to growth in 2025.”

“launching unsupervised Full Self-Driving as a paid service”

Takeaway: Although the company looks more and more like a typical car company with its gross margins, the story of Tesla is not one of a typical car company. Elon Musk has been able to weave a beautiful story of Tesla being Waymo, NextEra, and OpenAI combined. This is why Tesla has been able to continuously avoid the scrutiny of the public markets because there is always another rabbit to point to. This quarter it was the promise of Full Self Driving combined with growth of its Energy generation and storage business.

My Take: I thought the stock would plummet once the earnings were released because vehicle deliveries declined all of 2024. But this is why I do not touch Tesla. There is just so much love and faith in Elon that it is extremely hard for real numbers to be allocated to this business. This company continues to be in my "TOO HARD TO EVEN THINK ABOUT" pile of companies.

But I love the fact that it gives me content to talk about.

Takeaway: Better than expected revenue growth but worrying signs as iPhone sales continue to decline.

📈Stock Move After Earnings: Stock ripped 4% after earnings but gave back all the gains as the earnings report was digested by investors.

🔢By The Number: Overall revenue increased by 4% to $124 Billion (insane that a company selling devices can make this much money in a quarter).

Profits increased 7% from 2023 to $36.3 Billion

iPhone sales fell 1% from 2023 to $69 Billion.

Driven by continued demand decline in China. Where sales fell 11% in the quarter.

Services revenue increased 14% to $26 Billion from the same quarter in 2023.

Gross margin increased to 46.9%. The highest level ever for Apple

Apple is expecting those margins to expand to 47.5% in the next quarter.

💬In Their Words: CEO Tim Cook said on the earnings call, “During the December quarter, we saw that in markets where we had rolled out Apple intelligence, that the year-over-year performance on the iPhone 16 family was stronger than those markets where we had not rolled out Apple intelligence.”

Essentially blaming declining sales on its inability to entice users with AI in China where it is not allowed.

My Take: I used to refer to Apple as the King of all companies. But the issue with being king is that everyone wants your crown, so you have to defend your position. However, you cannot move your castle because that might leave room for competitors to take the throne. We can see this playing out with Apple's pickiness in what business lines it tries to take over. It has been way more controlled in its AI choices when compared to a company like Microsoft which has taken a pray-and-spray approach. Microsoft has invested in a ton of companies and incorporated AI into its products before they were fully ready.

Apple is no longer a growth engine. It is now more like a Wal-Mart. Apple is a staple of most households when a phone or computer breaks, more than likely an iPhone or a Mac will be purchased for replacement. This is why Apple can maximize its profitability (gross income increasing) while other tech companies are still in growth mode.

Not Financial Advice: Apple was my first-ever stock and the largest holding in my single stock portfolio. However, over the last 5ish months, I have been selling portions of my stake as the stock has been ripping. Apple is now a very safe company that can guarantee you returns via dividends and share buyback (spent $30 Billion on it in Q4 2024). However, I get safely by buying index funds. When buying single stocks, I am looking for companies with the best risk-return growth. Hence ASML entering the portfolio.

I might be wrong I'm probably wrong. I have no idea what the future holds. Apple makes more than $100 Billion a year from services which might be the path towards future growth. Any other business making that much would be seen as unbelievable. But with Apple, it's seen as almost pocket change because of $60-80 Billion a quarter from iPhone sales.

That's why I don't sell all of my holdings but just parts. I'm greedy. I want my cake while at the same time, I wanna eat it too.

Stats of the Week

The percentage of people making ONLY the minimum payment on their credit cards. It is the highest level since 2012, according to the Philadelphia Federal Reserve. There has also been a 10% increase in the number of accounts with balances overdue by a month.

It seems the higher interest rates on credit cards are having a larger effect on the ability of many to be able to pay down their balances. The average interest rate on credit cards is 21.5%. Which is A LOT of money.

Takeaway: Things are still okay for consumers but signs are showing that there is not a whole lot more room for consumers to take on more debt.

Expect a lower raise than you got last year.

According to a survey from Gartner, CEOs expect to raise salaries less than they have in the last 3 years as they move things back to pre-pandemic levels. With an increased difficulty in switching jobs, companies have the power back in their hands to hold pay lower than they otherwise would have to.

My Takeaway: 1 is greater than 0.

To advertise during the Superbowl, will cost you $8 million. The even bigger deal is that FOX is completely sold out of advertising space. Last year it was $7 million for an ad spot. It is crazy how much money can be charged for Super Bowl ads.

However, it makes sense. The Superbowl is pretty much the last place where all of America watches the same thing. Last year, 123 million people watched the Superbowl. It is expected that even more people will watch the Super Bowl this year.

For businesses trying to get customers, the Superbowl is one of the best ways to get a mindshare.

📈15%

The average increase in car insurance across the US. In Georgia, our insurance is increasing by 20% on average. Still better than 58% in Minnesota or 53% in Maryland.

Why?: As cars have gotten more expensive, insurance have to shell out even more money for accidents. Plus, new cars are now computers on wheels which means it is more expensive to fix historically what would have been small damages like bumper-to-bumper collisions.

Also increases in natural disasters mean insurance has to replace cars far more often. Then there are the additions of electric vehicles on the road.

Takeaway: I thought I would be seeing cheaper insurance after turning 25 years old. But that ain't happened once!

Looking Ahead

It’s gonna be a jam-packed week ahead. A combination of earnings and big economic data.

Jobs Data

On Wednesday, we get ADP’s Private payroll.

On Thursday, we get weekly jobless claims.

On Friday, we get the Big Daddy, the nonfarm payrolls.

Company/Earnings

Google reports on Tuesday

Disney on Wednesday

Amazon on Thursday

Sports I Love

⚽NO….WORDS

😲🤯WHA

Extras

The learning losses due to the pandemic where kids were forced to be out of school are mounting to much greater levels than ever expected.

In Their Words: The US Department of Education said, "Not only did most students not recover from pandemic-related learning loss, but those students who were the most behind and needed the most support have fallen even further behind."

However, this is not just a pandemic story. Pegg G. Carr the commissioner of the National Center for Education Statistics, points to the fact that the decline has been happening since 2017. She points to the rise of screens and devices that kids are on almost 24/7.

*I am a tiny shareholder in this company.